TOKYO — The collapse of the US-Iran ceasefire is hitting Asia hard. Again.

The region never really left the woods. It had been bracing for second-round shocks — surging food prices chief among them — so the calm around the Strait of Hormuz felt less like a resolution than a reprieve.

And that reprieve just ended. As US President Donald Trump made clear this week, the “peace deal” between Washington and Tehran was more of a vibe than a treaty.

Few investors are shocked by the resumption of hostilities. Trump’s pattern — escalate, back down, escalate again — is well documented by now.

But there’s a gap between war continuing in theory and war continuing in practice, and Asia is living in that perilous gap. Making things worse: gold, the trade Asian central banks had been piling into, is sliding fast and hard.

“The ceasefire between the US and Iran was always fragile, and some flare-ups were inevitable, unfortunately,” says Ryan Sweet, chief global economist at Oxford Economics. “The question is whether this represents a bump in the road or whether we’re emerging from the eye of the storm.”

His warning: “If the peace deal breaks, and it’s too early to tell, it won’t just raise oil prices. It would also increase pressure on AI supply chains in Asia, force central banks to be hawkish, tighten financial conditions, and could shift the outcome of the US midterms. The cascade runs fast.”

Asia sits squarely in that cascade’s path. China’s economy is losing steam as global demand cools and supply chains snarl. Japan’s stagflation problem is getting messier, with inflation running more than five times the 0.5% growth the Bank of Japan projects this year.

South Korea, which sources roughly 70% of its oil from the Middle East, is exposed on the logistics front — the Bank of Korea sees inflation staying above 3% even with the bombing paused. India’s rupee has fallen to record lows as markets punish New Delhi’s twin deficits.

Indonesia is fighting its worst currency-speculator siege since the 1997-98 Asian financial crisis, for similar reasons. Both the Reserve Bank of India and Bank Indonesia are intervening heavily.

The Philippines is propping up the peso too, with an impeachment vote against Vice President Sara Duterte — amid her ongoing feud with President Ferdinand Marcos Jr. — adding political noise to market stress. All of these fault lines could reopen as Trump’s Gulf war grinds on.

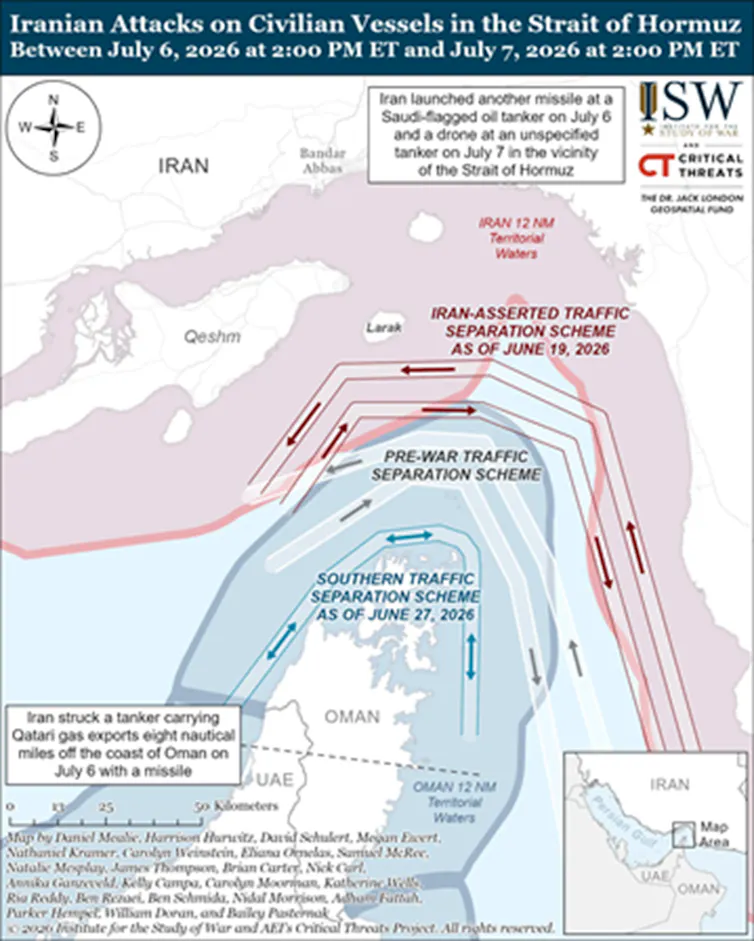

As Eurasia Group CEO Ian Bremmer puts it, control of the Strait of Hormuz “has always been the haziest part of the ceasefire. Washington insists the waterway should be fully open, while Tehran still exerts functional control over it. Still, neither side would seem to want a return to full-scale war.”

Whether that holds is really up to one man. “In the US,” Bremmer notes, “the war is already deeply unpopular among the public. The Iranian regime, meanwhile, has already demonstrated its resilience and secured at least a pathway to a negotiated solution — it would have little to gain from a return to open-ended hostilities. That, at least, is the cold analytical take: will both sides see things so rationally in reality?”

Markets are still waiting for that answer. This week, the IMF raised its 2026 headline inflation forecast to 4.7%, based on energy prices that were roughly 25% above pre-war levels as of February 28. If the Middle East slides back into chaos, that number is already stale.

Gold’s reversal adds another wrinkle. The People’s Bank of China bought 15 tons of it in June alone — its biggest monthly purchase this year and a 20th straight month of buying. Whether that counter-cyclical bet, echoed by other Asian central banks, pays off remains to be seen.

For now, spot gold sits near $4,100 an ounce, more than 20% off January’s record of $5,594.82. Part of the retreat traces to the Fed’s hawkish turn: the FOMC came out of its June 16-17 meeting leaning toward hikes, not cuts.

In its annual Central Bank Gold Reserves survey, the World Gold Council found that a growing number of the 74 monetary authorities it polls plan to increase gold reserves over the next year amid deteriorating geopolitical conditions. Roughly nine in 10 central banks expect gold reserves to increase over the next year; 45% say their own holdings will grow.

“This underlines that institutional interest is geographically widespread and that global price dips are being used to strategically build up reserves,”says Bjorn Junker, a commodities analyst at GoldInvest.

Despite dollar strength, Junker points to an “undisputed trend towards de-dollarization. As soon as oil-producing countries start recording higher revenues again, it is expected that this capital will flow less into US government bonds and instead increasingly into the gold market.

For central banks worldwide, the precious metal thus remains an essential strategic component of their reserves, the long-term accumulation of which is consistently pursued during price declines.”

Yet there’s plenty of two-way flow in investment circles, given how stubbornly the dollar is standing its ground — and gold isn’t.

Carol Kong, economist at Commonwealth Bank of Australia, says that “if we’re right about this conflict being protracted, oil prices will just keep rising and it will push the dollar higher, at the expense of net energy importers like the Japanese yen and the euro.”

Here, the Fed’s about-face is a sharp reversal from what markets expected of new Chair Kevin Warsh, who ran his first Federal Open Market Committee (FOMC) meeting last month. Trump picked Warsh as the anti-Powell — the man who’d cut rates early and often.

Instead, May’s inflation print — 4.2% year-on-year, up from 3.8% in April and the fastest pace in three years — has left Warsh almost no room to deliver. The result: a Fed tilting hawkish just as the dollar was already running hot.

By any normal logic, the last six months should have been brutal for the dollar — tariffs, fiscal blowout, military adventurism, debt barreling toward US$40 trillion. Instead, global investors seem to be doing what they always do eventually: regressing toward the mean.

From an interest-rate-differential standpoint, there’s an argument favoring the dollar in this frenetic environment. But the de-dollarization logic making the rounds in recent years — especially since the Trump 2.0 era began in January 2025 — hasn’t fallen away.

In a May survey of family offices worldwide, UBS found interest in avoiding the dollar on the rise. “Last year, all of the family offices were super concerned about global trade tariffs tensions,” notes John Mathews, head of private wealth management at UBS.

“Today it’s really shifted to geopolitical tensions around the world, global debt, and now interest rates. And not just the short-term implications, but the longer-term implications of these as well,” Mathews said.

These forces, he adds, “point to preparation not just for near-term volatility, but for an extended period of elevated and interconnected risk. Family offices look to be focused on building resilience across a broader and more complex risk landscape, combining adjustments to their asset allocation with multishoring strategies.”

In other words, dollar skepticism remains. But the numbers keep showing that rumors of the dollar’s demise are, for now, greatly exaggerated. In fact, “the King Dollar is no longer just firming — it’s starting to behave like a wrecking ball across Asian FX, equities and gold,” notes Stephen Innes, managing partner at SPI Asset Management.

“King Dollar is back in the driver’s seat, and the ride is getting rougher for the parts of Asia that had grown accustomed to the old market assumption that the Federal Reserve would always keep one hand near the punch bowl,” Innes says. “That assumption is now the market’s most obvious Achilles’ heel.”

The reason, Innes explains, is that “markets no longer treat the Fed as a friendly bartender quietly topping up the liquidity bowl whenever risk assets wobble.” The possibility that Warsh’s Fed could deliver one or two “servicing hikes” next year, he notes, rather than a dramatic tightening cycle, is enough to keep the dollar “well bid and likely rally further.”

All this is reshuffling Asia’s calculus at bewildering speed. Currencies across the region are cracking — the yen, the rupee, the rupiah, now the peso and baht too.

The common threads are surging oil prices and a muscular dollar punishing exchange rates almost everywhere, keeping governments from Tokyo to Jakarta on daily intervention watch and forcing central banks into hikes their populations can barely sustain.

The cruelest twist: Iran-war risk is re-emerging just as AI sends Asian stock valuations to nosebleed levels. The Kospi is up 77% year-to-date; the Taiwan Stock Exchange, 56%. This week, SK Hynix is raising $26.5 billion in an American depositary receipt offering — the largest-ever US share sale by a foreign company. It’s timed to a moment of maximum market volatility. Boom and bust, it turns out, can share a currency.

But even worse for Asian governments is not knowing what they don’t know about where the Iran war the US and Israel started might be headed.

Trump answering a reporter’s question this week about just that “I don’t know” isn’t promising for Asia’s second half of 2026. À lack of fiscal space post-Covid to stimulate growth is complicated by central banks under pressure to defend sliding currencies with rate hikes.

Asia had hoped for a quieter second half of 2026 as cooler heads prevailed in Washington and Tehran. The region’s economies aren’t going to get it.

Follow William Pesek on X at @WilliamPesek

{kind=link}

{kind=link}

{kind=link}